How do we protect our family?

They say the only certainties are death and taxes. But we know that change is also a constant in our lives, and we can build our capability to deal with changes over time.

Protecting our families, from a financial perspective can mean different things to everyone. Strategically, it needs to contain four key elements:

Living sustainably - ensuring we earn more than we spend

Having cash on hand - a cash buffer to deal with small and moderate curve balls that life will throw at us

Avoiding debts - ensuring we’re not weighed down by crappy debts like credit cards and personal loans

Plan B - protecting ourselves via insurances for significant and financially disruptive life events

A good offence is as important as good defence, and you need to have both working in unison to be financially healthy. Having a rock solid back up plan will allow you to take risks in order to grow.

Let’s explore what it means to have an effective Plan B (in the context of insuring your life, not your iPhone).

Insurances are rarely enjoyable to talk about (unless you’re an adviser), but understanding what role they play and how they can make sense for you, can improve your relationship with them and the value they provide.

As an adviser, I routinely assess my clients lives using a handy tool called an Insurance Needs Analysis. This allows us to discuss the risks that are relevant to them, and summarise what we are trying to protect when it comes to an insurance strategy.

Reviewing a Needs Analysis is an important exercise to do regularly, but it is even more important to do when life presents you with a catalyst. Taking on substantial debt, realising an asset, changing your income (up or down) are common prompts. But nothing looms as large as the introduction of a tiny human to make us sit up and pay attention to what would happen if the proverbial hits the fan.

For the majority of my clients, there are four types of personal insurance that are relevant: life insurance, total & permanent disability (TPD) insurance, trauma (or critical illness) insurance and income protection (or salary continuance). They all play different roles and address different needs.

When we start or grow our family, naturally, our needs change.

The major changes are in our lump sum needs, or our life and TPD needs.

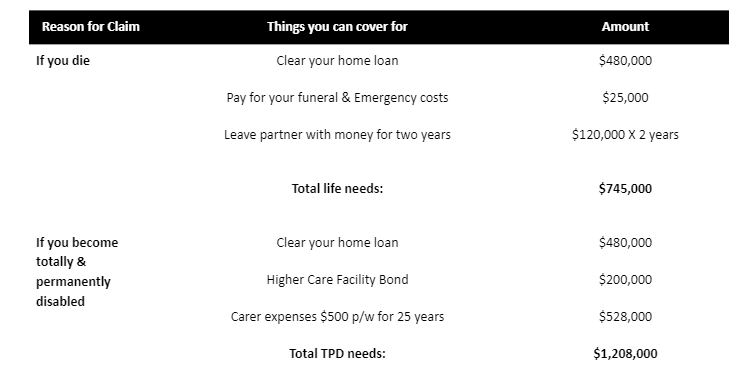

Prior to having children, here’s an example of what a Needs Analysis could look like for a professional couple.

This is not dissimilar to where Mr. Pritchard and I were a few years ago - we wanted to know that if something happened we could cover our debts (and therefore not be pressured to sell assets or be uprooted from our home) and that we wouldn’t ‘need’ to go back to work straight after an emergency.

But what was an acceptable plan for us as a couple, didn’t really cut the mustard as a family. This was particularly relevant around the flexibility (or requirement) of returning to work after a calamity and that the success of our goals required two incomes over a number of years.

Therefore, our needs increased with the introduction of dependents.

I’ve highlighted some changes that could be prompted after having two children.

* This is on the assumption that the individual also had an income protection policy in place that would be triggered in the event of a TPD claim.

There’s no right or wrong way to assess insurance needs, and the above is an example only.

For some families, including spouse support alongside the cost of living for children is critical. For others, less so. Other families may want to include investment debt as well as debts on their main residence. Perhaps the education costs need to be substantially higher to factor in private education.

The aim of the above is that it is a conversation prompt, and a framework for considering your needs. It helps us move from the realm of “$1.0 million sounds like a nice amount of insurance” into something meaningful and relevant for our lives.

We can then reconcile these needs against our current insurance coverage, which may range from nil to excessive, to work out what needs to be changed. Likely, we will need to apply for or increase our insurance to meet our needs.

This will ensure we’re not paying for insurances that we do not need. Equally as important, it will ensure we are not exposed to risks that will be financially crippling to our families.

Regular review of your insurance over time may allow you to decrease your cover as your needs reduce and/or your wealth grows.

A challenge advisers routinely face is where the insurance strategy is a reflection of the earnings of the couple, rather than the value they provide to the family. Let me speak plainly: a stay-at-home parent (often the mother) is as important to insure as a breadwinner. When it comes to the death or substantial disability of a parent, particularly where there are young children, it does not matter which parent is impacted - either will result in a financial disaster if quality insurances are absent.

There are two reasons for this.

Firstly, the importance of unpaid work in the home (whether it is for raising the family or domestic responsibilities) is often overlooked, but financially significant. If an individual is unable to perform that role due to death or disability, this will likely substantially impact the partner’s ability to work and/or increase costs as those responsibilities are outsourced.

For example: if you have two children who are currently cared for at home, but after a death or disability they enter full time childcare, that could be an increased household cost of $39,000 p.a. (based on $75 per day net of childcare rebates).

Secondly, when it comes to disability, the reasons above are relevant and then there are a whole lot of additional costs thrown on top. Medical and rehabilitation costs, carers, alterations to your home are common. Losing an income and having an increase in expenses, both upfront and on an ongoing basis, can be overwhelming.

Death, critical illness or significant disability are incredibly challenging life events to navigate. But by having a proactive and pragmatic conversation as a family, they do not need to be a financial challenge as well.